Overview:

What is Accounting? Webster’s Dictionary defines accounting as: “The system of recording and summarizing business and financial transactions and analyzing, verifying, and reporting the results”.[1]

Purpose:

This article will give some of the basic key principles of accounting. There are many forms of accounting, but for now, we’ll talk about the United States of America Generally Accepted Accounting principles, US GAAP. However, most forms of accounting, such as International Financial Reporting Standards (IFRS) (which is used in many countries), have similar principles.

The first decision to make in accounting is if you want to account for your business (or personal life) as cash or accrual basis of accounting. Cash basis accounting is based upon whether you receive or pay cash. Accrual basis accounting is based upon when revenue is earned or the services are incurred and not when cash is received or cash is paid.

Analysis # 1:

Let’s do a quick example to show how cash vs. accrual basis accounting works. Let’s show how an individual accounts their monthly electric bill. You sign up for a new electric plan for October. You used the electric in October, but the bill was not due to be paid in cash until November. Under cash basis accounting, there would be no expense in October because there was no cash paid in October. In accrual basis accounting, since the electric was incurred in October, we would have electric expense in October and a liability due to the electric company. US GAAP requires the use of accrual basis accounting whereas US Tax returns usually use cash basis accounting.

Analysis # 2:

Now that we’ve discussed the differences between cash and accrual basis accounting, let’s go into other key principles of accounting.

Some key terms in accounting:

– T Account – Tracks all the debits and credits and allows anyone to see what the balance in an account at any point in time.

– Debits – Left side of a T Account, shown as a positive.

– Credits – Right side of a T account, shown as a negative.

– Assets – these are things we own. They hold a debit balance and some examples of common asset accounts are: Cash, Account Receivable and Fixed Assets.

– Liability – these are what we owe others. They hold a credit balance and some examples of common liability accounts are: Accounts Payable, Mortgage Liability and Interest Payable.

– Equity – this is the company’s or individual’s net worth. They hold a credit balance if we have positive net worth or a debit balance if we have a negative net worth. Some examples of common equity accounts are: Dividends, Net Income and Common Stock.

– Revenue – these are income to the company. They hold a credit balance and some examples of common revenue accounts are: Sales, Interest Income and Gain on Sale.

– Expense – these are costs to the company. They hold a debit balance and some examples of common expense accounts are: Cost of Goods Sold, Marketing Fees and Interest Expense.

– Any revenue and expense accounts roll into our equity account called Retained Earnings. Thus, all accounts that are part of the “Income Statement” (revenue & expense) will be part of equity.

The most important principles (done as equations) are:

1) Assets = Liability + Equity

2) Debits = Credits

Overall accounting is based upon a 2-line entry system of a debit and a credit. Each time we make a journal entry we are either increasing or decrease the balance of an account.

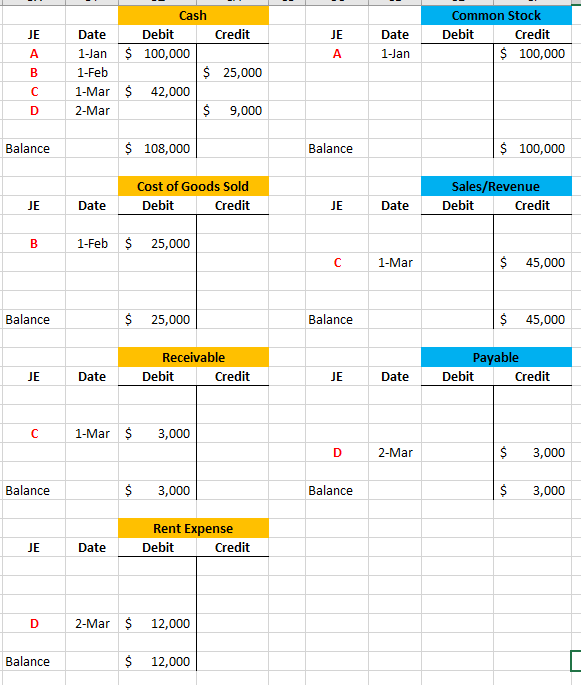

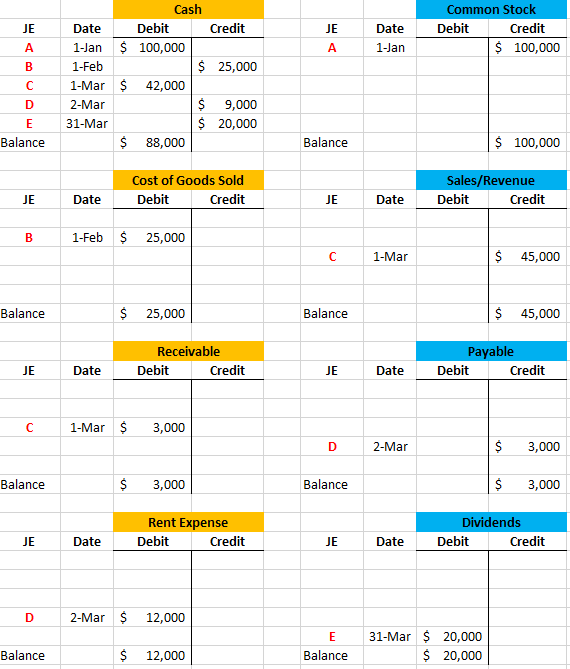

Analysis # 3:

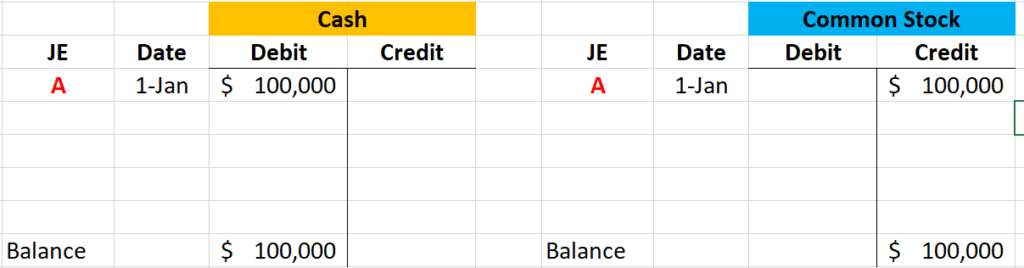

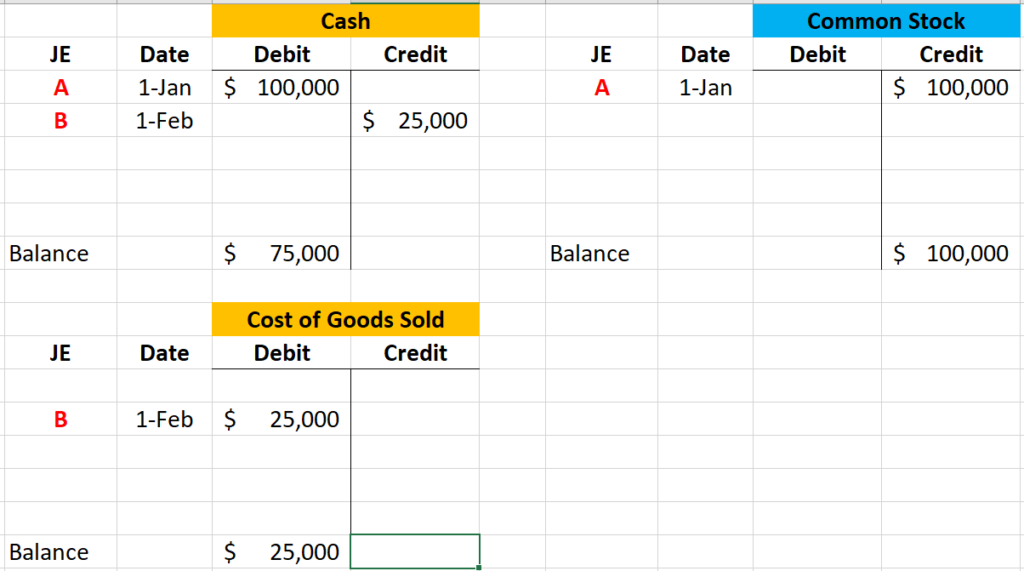

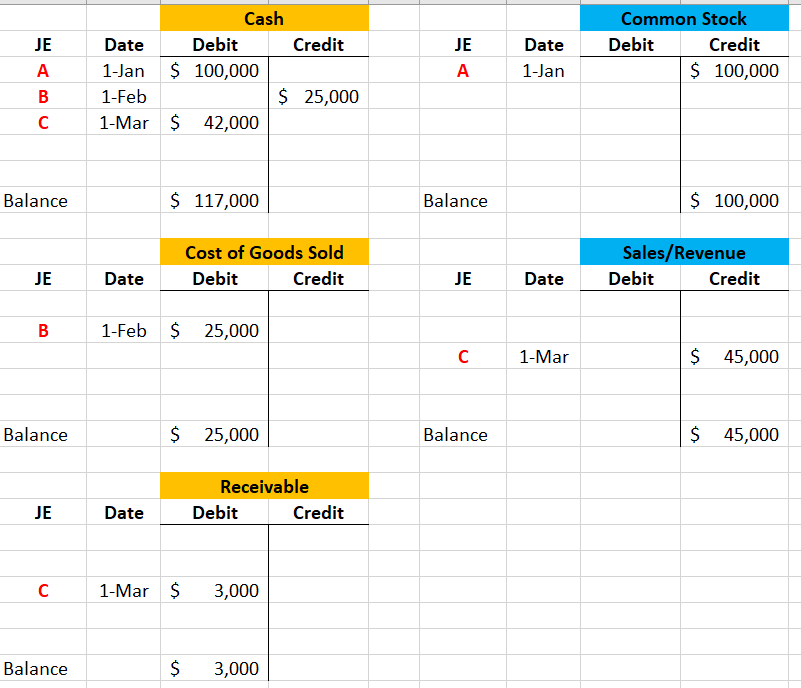

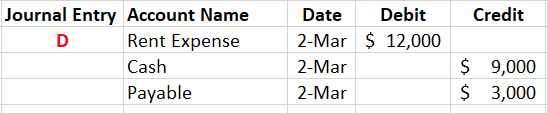

In order to see this in practice, let’s walk through a couple entries of our MFC Pizza Company.

A) On January 1st, you will start the company with a $100,000 cash investment. The company has received an asset of cash. Assets increase by debits; thus, we will debit the cash account. We now have cash (investment/equity) in our business and we will increase equity which is done by a credit to Common Stock (or Equity) account.